Ecological Accounting

Why ecological accounting

There is increasing desire to account for "externalities" from human production and transportation processes, and certainly the need has always been there. Related, there are also more efforts to do "climate accounting" on a global level, to provide knowledge in the efforts to improve the situation, which is spiraling out of control on many levels - climate chaos, soil and biodiversity loss, uncontrolled emission of substances on the land and in the water toxic to life, etc.

There are many reasons this has not been part of the accounting paradigm, including interests of corporate players and tendencies of industrial era humans to think about "the environment" as something separate from us, from which we can extract resources without regard to the many interconnections. Although there are some efforts to give ecosystems rights relative to human impact, and helpful ways to think about the issues from indigenous sources and people working on the "commons", a large "paradigm shift" will be needed and there is much inertia and resistance.

As always, our goal is to give Valueflows the latitude to support both conventional and next economy accounting. The latter will more and more involve ecological accounting.

So, understanding there will be much more learned going forward in practice, we want to make Valueflows broadly supportive of these efforts. In general, this can be a step forward in being able to broaden our ability to do the accounting we need to do to confront the current climate and biodiversity challenges.

See also Accounting.

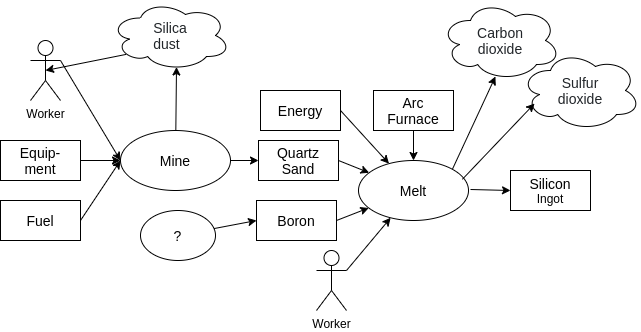

REA IPO resource flows

The Valueflows input-process-output REA resource flow model works very well for ecological accounting, with some broadening of our thinking about agents and resources, and what "economic" entails. If we think of "economic" as broader than human activity, which has tentacles into most if not all of the other ecosystems on earth, it becomes easier to consider "accounting" in light of flows to and from those ecosystems, all of which eventually affect human economies.

This rough diagram shows some of the flows for solar panel production. Silica dust is an output of the mining process, which gives mine workers silicosis. There are many additional flows here which could be detailed to go into and out of ecological ecosystems, affecting them and also humans.

Economic Resources

We have thought of economic resources as having use value (and sometimes exchange value) to humans and ecosystems. If we broaden that to include "bad" as well as "good" resources, we can model more completely and accurately the resource flows that impact ecosystems including humans. It is also not very helpful to even think in terms of "bad" and "good" as part of the definition, since that is conditional. For example, CO2 is "good" for plants in a greenhouse, but "bad" pumped into the atmosphere, and some of the CO2 in the greenhouse will leak out, making it "bad"... yet it is the same substance.

Agents

We have defined Agents as people and organizations (formal or informal). If we go beyond human-centric thinking, we could conceive of Agents as other living things, and also as groups of other living things, or whole ecosystems. Those ecosystems could be of any size or complexity, and all types of agents could have various relationships between each other and their ecosystems. For example, a lake receives and provides many economic/ecological resources, for example nitrogen from farm runoff, water and habitat for living things.

This requires some things which are traditionally considered by humans to be resources, to be considered agents in their own right. We understand that some living things (say beef cattle being raised by a farmer) need to be accounted for as resources, and Valueflows will of course continue to support that. On the other side of the puzzle, we also realize that we could consider a human being as an ecosystem, given the microbiota that lives there and even influences behavior. So, the goal is to keep the model simple and flexible enough to support current practices, while also supporting continuing exploration and expansion of our thinking about agency within the global ecosystem of living beings.

But how can these non-human agents give input to human accounting systems? One way is through sensors; another is through human "representatives". Of course, this is all still unavoidably human-centric. Some ecological agents need human agents to represent them in human governance activities, similar to specific humans representing organizations. This idea has both supporters and opposition: Federal Judge Strikes Down Lake Erie Bill of Rights. And there are evolving experiments to refine how humans can act on behalf of ecosystems, and to include indigenous groups who have had responsibility going back centuries. There are many ethical, legal, and practical considerations, but we think it is important to support our human desire to account for climate change and for harm from externalities.